Not long ago you only saw the barrage of Medicare Advantage television commercials in the period leading up to Medicare Open Enrollment.But now those promotions run year-round, offering a confusing and sometimes misleading array of plans sponsored by a variety of health care companies.Adding to the confusion is the fact that many people dont fully understand the difference between Original Medicare and the Medicare Advantage plans.Each has advantages and disadvantages, and you need to understand them before you make your choice.Get Ready for Open EnrollmentThat will be critical for Medicare Open Enrollment, which runs Oct.

15 through Dec.7.Thats when you can switch plans if you choose (though most people dont switch.) Meanwhile, Medicare Advantage Open Enrollment runs Jan.

1 through March 31 every year.Medicare ExplainerYou are eligible for Medicare when you turn 65 (earlier if they have certain disabilities).You can sign up during general enrollment, which runs Jan.1 through March 31, and is not to be confused with Open Enrollment for existing Medicare customers.

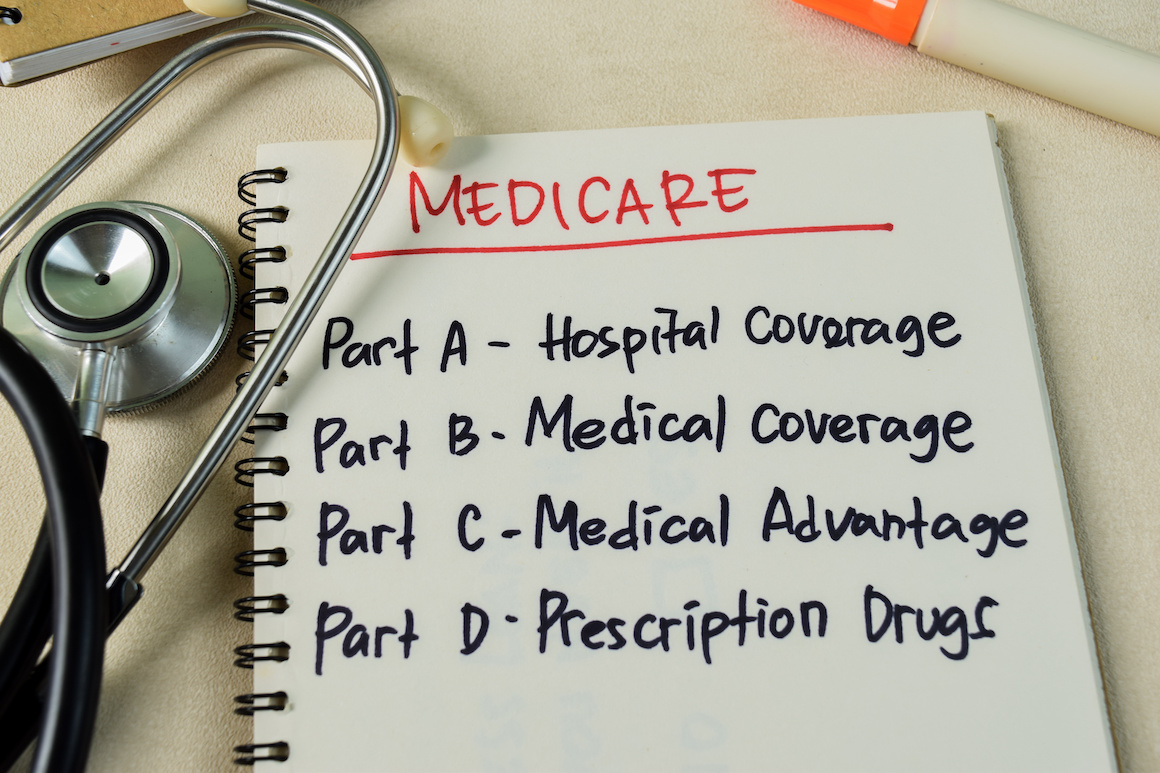

Seventy million Americans depend on Medicare as their primary insurance.Medicare Parts A & B are considered Original Medicare, which is run by the federal government.Part A covers inpatient care provided by hospitals, skilled nursing facilities and hospice.Part B covers outpatient expenses, including doctors offices and clinics.

You can choose any doctor except those who opt out of Medicare entirely.Part D must be purchased separately and provides coverage of prescription drugs.The Medicare Advantage Plans, meanwhile, are sometimes referred to as Part C.These plans are run by private insurance plans contracted by Medicare and not by the government.

These policies may include prescription drug coverage, as well as dental, vision and hearing insurance none of which are covered by Original Medicare.However, the Medicare Advantage Plans restrict your choice of the doctors.Which to Choose?The answer is it depends.While both traditional Medicare and Medicare Advantage have pros and cons, it is important to consider how each option aligns with your financial goals, anticipated healthcare expenses and overall retirement budgetand re-enrollment is quickly approaching in November, says Kelli Smith, Director, Financial Planning at Edelman Financial Engines.Original MedicareProsProvider flexibility.You can see any health care provider in the country who accepts Medicare, and nearly all of them do, says Moeller.

The challenge is to find somebody who can give you an appointment.No prior authorization.Most services dont require navigating complex approval processes, saving time and avoiding potential delays in receiving care, Smith says.Medigap coverage.Medicare does not cover 100% of Part B costs, but the option to purchase a Medigap policy is available.

Medigap is extra insurance that you buy (details here), to help cover potential out-of-pocket expenses, says Smith.ConsNo out-of-pocket limit, meaning significant costs could arise if frequent or costly care is necessary.It does not pay 100% of part B expenses.Many people with Original Medicare also get a Medigap supplement plan, because while Original Medicare has pretty extensive coverage, it doesnt pay 100% of all the things it covers, says Moeller.The biggest hole in Original Medicare is that it only pays 80% of Part B expenses.

Twenty percent of a big number, so many people, especially those of some financial means, tend to favor a Medigap plan that helps close those gaps.Fewer benefits.You pay separate premiums for drug coverage.To get prescription drug coverage you must pay for a Part D plan.

Also, Original Medicare does not include vision, dental or hearing insurance.Multiple insurers.You have to deal with multiple insurers for your benefits.You deal with Medicare for Parts A&B, another insurer for Part D prescription drugs, and still a third for your Medigap coverage.Traditional Medicare is proper goal for people who can afford the Medigap premiums.

If you have a Medigap plan, its possible to find a plan that closes nearly all of the spending gaps in traditional Medicare., says Philip Moeller, author of the updated Get Whats Yours For Medicare, out Oct.8.Medicare Advantage Medicare Advantage plans, meanwhile, cover Parts A and B, but most of them also cover prescription drugs, which are available in Original Medicare separately, under Part D prescription drug plans.Theyre very attractive for people who dont have a lot of money, says Moeller.Theyre very attractive for people who dont have heavy health care spending needs, and theyre very attractive for people if they have provider networks that contain the physicians that you already see.ProsLower costs.

You dont need Medigap coverage.Also, these providers bid for a contract to provide services to Medicare patients and normally underbid some of their costs, says Moeller.And the government provides a subsidy that allows them to offer more benefits.More supplemental benefits.

Many Medicare Advantage plans provide zero-cost Part D drug plans that many people like, says Moeller.Other benefits can include routine hearing, vision and dental care, and theres some other supplemental benefits, like gym club memberships and things like that.The list of supplemental benefits is growing as healthcare insurers discover that theres a lot of so called non-medical benefits that have a really strong correlation with your health.Less paperwork.

Administratively, you only have to deal with one insurer for all of your healthcare needs, says Moeller.ConsLimited choice of doctors.You cant see any doctor.You usually are restricted to see doctors in the network of care providers that have been set up by the particular Medicare Advantage plan you enroll in.

The plans do this because it allows them to save money.Prior Authorization.Medicare Advantage plans are whats called managed care, which means that they have a play a strong gatekeeper role in getting access to care.This, they say, is a cost-saving measure and a protection against people getting care they dont need.

However, this process, which is known as prior authorization, has been a real headache for everybody, says Moeller.Doctors dont like it because it generates tremendous paperwork, and the plans have gotten a lot of pushbacks from both the public and healthcare providers, and more lately, from Medicare itself, which has received a lot of complaints.Today 54% of eligible Medicare recipients have chosen Medicare Advantage plans.I think the big draw is the costs, Moeller says.

Healthier people in their 60s and 70s tend to like Medicare Advantage because they dont have substantial health needs right now, and so they save a lot of money on Medicare Advantage.They dont seem to be disadvantaged substantially by the limitations of prior authorization, or of the fact that they have to deal with a system of network providers.YOUR TURNWhich do you prefer original Medicare or Medicare Advantage? Let us know in the comments!Rodney A.Brooksis an award-winning journalist and author.

The former Deputy Managing Editor/Money at USA TODAY, his retirement columns appear in U.S.News & World Report and SeniorPlanet.com.He has also written for National Geographic, The Washington Post and USA TODAY and has testified before the U.S.

Senate Special Committee on Aging.His book, The Rise & Fall of the Freedmans Bank, And Its Lasting Socio-economic Impact on Black America was released in 2024.He is also author of the book Fixing the Racial Wealth Gap.

His website iswww.rodneyabrooks.comYour use of any financial advice is at your sole discretion and risk.Seniorplanet.org and Older Adults Technology Services from AARP makes no claim or promise of any result or success.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by Senior Savings Deals.

Publisher: Senior Planet ( Read More )

Publisher: Senior Planet ( Read More )